| HFT Breaks Speed-of-Light Barrier, Sets Trading Speed World Record. Adds a new unit of time measurement to the lexicon: fantasecond. |

Back to Main Research Page  |

On September 15, 2011, beginning at 12:48:54.600, there was a time warp in the trading of Yahoo! (YHOO) stock. HFT has reached speeds faster than the speed-of-light, allowing time travel into the future. Up to 190 milliseconds into the future, or 0.19 fantaseconds is the record so far. It all happened in just over one second of trading, the evidence buried under an avalanche of about 19,000 quotes and 3,000 individual trade executions. The facts of the matter are indisputable. Based onofficial UQDF/UTDF exchange timestamps, there is unmistakable proof that YHOO trades were executed on quotes that didn't exist until 190 milliseconds later! Millions of traders depend on the accuracy of exchange timestamps -- especially after bad timestamps were found to be a key factor in the disastrous market crash known as the flash crash of May 2010. We are confident the exchange timestamp problem has been completely addressed by now: the SEC would have made sure of it. Adding accurate timestamps is not exactly rocket science; it's not even considered to be a difficult problem. Based on recent marketing materials, the exchanges are practically experts on measuring time. And with hundreds of millions in annual data feed subscriptions paid by the same subscribers expecting quotes with accurate timestamps, there is no shortage of funds to make it happen. So we can be certain the exchange timestamps were accurate, which means that HFT has truly entered the era of the fantasecond. But let us suppose for a moment that in reality, quotes became queued (delayed) and were timestamped after leaving this queue. After detailed analysis of the UQDF data feed (see chart below) that transmits this information to traders, we find that the traffic rate for all output lines and specifically multicast line #6 which carries YHOO, were well below peak rates. So it doesn't appear there were any capacity problems which have always been an excellent indication of feed delay. This raises a few thorny questions. Does this mean there are far more delays than previously thought? Is there a delay every time we see an explosion of quotes in one stock? Because recently, that, sort, of thing, happens, all the time. Regulation NMS (Reg. NMS) makes it clear that direct exchange feeds are prohibited from having a speed advantage over the UQDF data feed. The reason is primarily because UQDF computes the NBBO, which is the key component of Reg. NMS that assures investors they are getting the best price when buying or selling stocks. This assurance is called trade-though price protection. How does one ensure trade-through price protection if the price being protected hasn't even occurred yet? Maybe it would be better to just fantasize about fantaseconds after all. |

{kind=link}

{kind=link}

| The first chart is a 250 ms interval chart of the NBBO in YHOO which is plotted as vertical lines and colored red if the NBBO was crossed during the interval, yellow if it was locked, and gray if it was normal. The implied quote rate is shown as a histogram at the bottom and scaled in quotes/second. We will focus on the time shown in the black circle. |

| Zoomed in detail of above chart in 2 millisecond intervals. Note that this chart shows just 2.1 seconds of time. |

| The next chart includes trade executions which are plotted as dots or squares and sized according to trade size. A unique color and shape is assigned to each reporting exchange. What is unusual about this chart is that trades are reported ahead of quotes. The trades (dots and squares) should trail after the quotes (vertical bars). Up to the point in time that is labeled A, and after the point labeled B, trades and quotes were in sync. Between these two points, quote timestamps began falling behind. |

| By plotting quotes and trades from just one of the active exchanges, we can easily measure how far in time the trade messages came before the quotes and therefore estimate the minimum amount of time the quotes were delayed. Below is a 1 millisecond interval chart of YHOO showing only Nasdaq trades (black circles) and the Nasdaq bid-ask spread (gray vertical bars). Note that this chart shows just over 1 second of time. |

Exchange Code Legend:

| 1 | NQEX | Nasdaq Exchange |

| 7 | PACF | NYSE/ARCA |

| 8 | CINC | National Stock Exchange |

| 9 | PHIL | Philidelphia Stock Exchange |

| 11 | BOST | Boston Stock Exchange |

| 60 | BATS | BATS Trading |

| 63 | BATY | BATS Y Exchange |

| 64 | EDGE | Direct Edge A |

| 65 | EDGX | Direct Edge X |

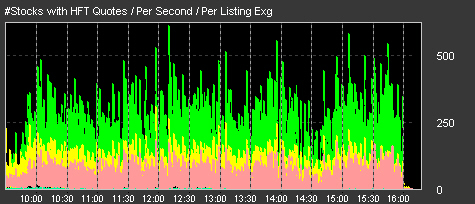

| The chart below shows quote message rates for UQDF and multicast line #6 which is the line that carries YHOO quotes. The time of the event is shown at the lower left. Although traffic from YHOO was a significant percentage of all traffic on UQDF, it was not high enough to indicate any problems. Note the much higher surge on the right side of the chart; there weren't any known problems at that time in YHOO. |

| http://www.nanex.net/Research/fantaseconds/fantaseconds.html |

No comments:

Post a Comment